Are you confident in accurately reporting cryptocurrency earnings on your tax returns?

IRS Clarifies Bitcoin Cash Hard Fork Tax Implications

April 20, 2021 · 2 min read

An IRS Memorandum released on April 9, 2021 clarifies when cryptocurrency hard forks are taxed.

The memorandum specifically uses the Bitcoin Cash hard fork as an example, which occurred on August 1, 2017 at 9:16 A.M ET. Pursuant to the hard fork, people who held bitcoin (BTC) received an equivalent amount of bitcoin cash (BCH). Although the fork occurred on August 1, 2017, not every BTC holder got access to BCH at that time. For example, people who used Coinbase had to wait until January 1, 2018 to get access to their BCH. Other centralized exchange users also had to wait several days or weeks before being able to withdraw their newly minted BCH.

Hard Fork Taxation

The IRS memorandum explains that a taxable event occurs at the time you gain dominion and control of an asset. In laymen’s terms, this means the taxable event occurs when a taxpayer has the ability to transfer the funds from a wallet or exchange — not at the time the actual hard fork occurred.

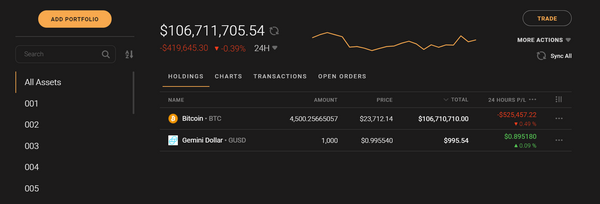

Let’s use an example to illustrate this. Say Jennet had 1 BTC on Coinbase on August 1, 2017. After the bitcoin cash hard fork, she was eligible to receive 1 BCH. On August 1, 2017, the price of BCH was above $400. However, Jennet was not able to access her BCH until Coinbase made it available on January 1, 2018. At this time, BCH was trading at approximately $2,500 on Coinbase.

In this situation, Jennet gained dominion and control over BCH on January 1, 2018. She must report $2,500 of ordinary income in 2018.

On the other hand, if Jennet held the BTC in a self-custodied wallet with her own private keys, she would have had ~$400 of income in 2017, resulting in a much lower tax bill. As they say, not your keys, not your coins.

Each time your portfolio goes through a hard fork, it’s important to check when your wallet or exchange supported the coin and when you received dominion and control to accurately figure out your income for tax purposes. A software tool like CoinTracker can help.

If you have any questions or comments about crypto taxes let us know on Twitter @CoinTracker.

CoinTracker integrates with 300+ cryptocurrency exchanges, 8,000+ blockchains, and makes bitcoin tax calculations and portfolio tracking simple.

Disclaimer: This post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.