Guide to India Cryptocurrency and Bitcoin Taxes (AY 2023-24 Edition)

May 5, 2022・9 min read

What is Cryptocurrency?

Cryptocurrency is a form of digital money.

Cryptocurrency is similar to cash, such as Indian Rupees (Rs) or US Dollars ($), but exclusively digital so there are no physical bills or coins. The first mainstream cryptocurrency, bitcoin, was created by a pseudonymous person called Satoshi Nakamoto in 2008. Since then, thousands of cryptocurrencies have emerged like Ether, Solana, and more.

In addition to being completely electronic, cryptocurrency has another unique property compared to other forms of money: it is not controlled by any central authority. The Bitcoin whitepaper describes how the decentralized protocol works without requiring any governments, central banks, or financial institutions.

Learn more about bitcoin and other cryptocurrencies in the Cryptocurrency 101 guide.

Is Cryptocurrency Taxed in India?

Yes. The Finance Act, 2022 states that cryptocurrencies and non-fungible tokens (NFTs) are classified as Virtual Digital Assets (VDAs) subject to taxes.

“ ‘Virtual digital asset’ means‒‒

(a) any information or code or number or token (not being Indian currency or foreign currency), generated through cryptographic means or otherwise, by whatever name called, providing a digital representation of value exchanged with or without consideration, with the promise or representation of having inherent value, or functions as a store of value or a unit of account including its use in any financial transaction or investment, but not limited to investment scheme; and can be transferred, stored or traded electronically”

(b) a non-fungible token or any other token of similar nature, by whatever name called;

(c) any other digital asset, as the Central Government may, by notification in the Official Gazette specify”

VDAs are a class of capital assets in the Indian tax code distinct from other classes of capital assets such as stocks and equity. The Finance bill makes cryptocurrency “transfers” taxable effective April 1, 2021. According to the Income-tax Act, Section 2, (47), a “transfer” includes (as related to crypto):

(i) the sale, exchange, or relinquishment of the asset; or

(ii) the extinguishment of any rights therein; or

(iii) the compulsory acquisition thereof under any law

There are two tax rates applicable to cryptocurrency income and profits:

- 30% flat income tax rate, effective April 1, 2022.

- 1% Tax Deducted at Source (TDS), effective July 1, 2022.

Note: the 2022 Finance act has only addressed high-level cryptocurrency taxation. The bill has not clarified taxation for other types of income such as staking, mining, lending, borrowing, DeFi, and other types of cryptocurrency transactions. Therefore, the tax implications below could vary as the Indian Revenue Service (IRS) issues more specific guidance in the future. For tax advice, please consult a tax professional.

Below are some of the common taxable events and likely tax implications based on the limited guidance issued so far.

Cashing out

Selling cryptocurrency and NFTs for INR (cashing out) is clearly a taxable event under the 2022 Finance Act.

Example: Arnav purchased 1 bitcoin (BTC) for Rs. 30,00,000 in 2020. He sold this bitcoin for Rs. 40,00,000 in 2022. Here, Arnav has to pay taxes on Rs. 10,00,000 (Rs. 40,00,000 – Rs. 30,00,000) of gains. The tax bill on this transaction will be Rs. 3,00,000 (Rs. 10,00,000 * 30%).

If an Indian exchange is used to cash out, the exchange may also apply 1% withholding taxes (TDS). TDS is a small tax amount exchanges collect from you and remit to the government. Continuing with the example above, if you are subject to TDS, the exchange may take out Rs. 10,000 (Rs. 10,00,000 * 1%) as TDS and only give you Rs. 39,90,000 (Rs. 40,00,000 – Rs. 10,000). You will pay the remaining tax bill of Rs. 2,90,000 (Rs. 3,00,000 – Rs. 10,000) when you actually file your taxes.

Trading and swapping coins & NFTs

Trading one coin/NFT with another is also a taxable event.

Example: Arnav purchased 1 bitcoin (BTC) for Rs. 30,00,000 in 2020. This BTC is now worth Rs. 40,00,000 today. He exchanged this BTC and purchased 1,000 ether (ETH) coins. Arnav has to pay tax on Rs. 10,00,000 (Rs. 40,00,000 – Rs. 30,00,000) of capital gains. The tax bill on this transaction will be Rs. 3,00,000 (Rs. 10,00,000 * 30%). Arnav may also be subject to the 1% TDS as described above.

Note that purchasing an NFT often requires you to trade/spend a cryptocurrency like ether. This transaction is also viewed as a trading/swapping event and taxed as described above.

Cryptocurrency & NFT gifts

Receipt of gifts up to Rs. 50,000 in a year is tax-exempt. If the gift is more than Rs. 50,000, the full value is taxable to the recipient at his/her slab rate. Subsequent sales of the gift would be subject to the 30% tax rate.

Note that the gift donor has no tax liability. Also, gifts from close family members on certain occasions are tax-exempt for the recipient.

Example: Arnav received 1 bitcoin (BTC) worth Rs. 10,00,000 as a gift. Since the gift amount is more than Rs, 50,000 Arnav has to pay taxes on this amount subject to his slab rate.

Mining income

Mining is the process by which Proof-of-Work (PoW) enabled cryptocurrencies like BTC first enter the circulation. Mining requires you to run powerful computers known as nodes. When nodes successfully solve complex mathematical problems in the blockchain, you receive mining rewards.

Although the bill has not explicitly mentioned how mining income is taxed, it is reasonable to assume that it is taxed at the time you receive the tokens.

Example: Arnav mined 1 BTC worth Rs. 10,00,000 in 2022. Arnav has to pay taxes on Rs. 10,00,000 of income subject to his slab rate.

Staking income

Crypto staking is a popular way of earning rewards by locking up coins that support the Proof-of-Stake (PoS) system.

Again, the Finance Act has not addressed how staking income should be taxed. Based on general tax principles, it is reasonable to assume that staking income is taxed at the time you receive staking rewards.

Example: Arnav received the following ADA tokens:

Arnav has Rs. 460 of total income which will be subject to his slab rate. If Arnav stakes through an exchange, he may also be subject to the 1% TDS.

2025

Crypto Tax

Guide is here

CoinTracker's definitive guide to Bitcoin & crypto taxes provides everything you need to know to file your 2024 crypto taxes accurately.

DeFi income

The bill has not mentioned how DeFi income should be taxed. However, going with the general tax principles, it is reasonable to say that DeFi income streams such as yield, interest, and other rewards are taxed as income at the time you receive them.

Here, Arnav has Rs. 210 of total yield income which will be subject to his slab rate.

Airdrops

Airdrops are free coins that you receive in your wallet. These are generally done as a marketing/publicity move by protocols to increase awareness of their token and you may not even know that this has happened.

Airdrops are likely considered gifts under the current rules. Gift receipts are taxed to the receipt only if it exceeds Rs. 50,000 in one financial year.

Example: Arnav received several APE coins valued at Rs. 55,000. If airdrops follow gift tax rules, Arnav will have to pay taxes on Rs. 55,000 subject to his slab rate.

Alternatively, if Arnav received APE coins worth Rs. 40,000, he won’t have to pay any tax.

Crypto earning from games and other sources

Cryptocurrency earnings through play-to-earn games and similar platforms will likely be taxed at the time you earn those tokens subject to your slab rate.

Example: Arnav earned 1 GAME token worth Rs. 1,000. Earning is a taxable event so he will have to pay taxes on Rs. 1,000 subject to his slab rate.

Cryptocurrency losses

Unfortunately, the current tax rules do not allow offsetting cryptocurrency losses against any type of income nor carry forward losses to future years. Therefore, if you incur any losses trading cryptocurrency, you will not gain any tax benefit.

Finance Act 2022, Section 115BBH –

“ (a) no deduction in respect of any expenditure (other than cost of acquisition) or allowance or set off of any loss shall be allowed to the assessee under any provision of this Act in computing the income referred to in clause (a) of sub-section (1), and

(b) no set off of loss from transfer of the virtual digital asset computed under clause (a) of sub-section (1) shall be allowed against income computed under any other provision of this Act to the assessee and such loss shall not be allowed to be carried forward to succeeding assessment years”

Nontaxable crypto transactions

Purchasing cryptocurrency & NFTs using Indian Rupees, hodling the assets, and sending assets from one wallet/exchange you own to another are not taxable events.

The Finance Act’s definition of VDAs is very broad. There are some concerns about cryptocurrency loyalty points and credit card rewards being classified as VDAs and subject to the 30% tax rate. According to government officials, these will not be treated as VDAs nor subject to the 30% tax rate. Regulators are planning to issue more specific guidance on this soon.

How does the Income Tax Department (ITD) know I have crypto?

Your cryptocurrency activity is not completely hidden from the tax regulators. There are many ways regulators know your interactions with cryptocurrency. One of the primary ways the Income Tax Department knows about your affairs with cryptocurrency is through the information that exchanges gather through Know-your-customer (KYC) policies and transmit as a part of TDS. Tax authorities can also demand exchanges to expose your activity in certain cases. They can also use blockchain analytics tools to catch crypto tax evaders.

When to file cryptocurrency taxes in India?

There are two time periods you need to remember when filing your taxes in India.

The financial year (FY) is the fiscal year in which you earn income. It goes from April 1 to March 31 in the following year. For example, the most recent closed financial year was April 1, 2021, to March 31, 2022. This time period is also shown as “FY 2021-22”.

The assessment year (AY) always comes after the FY. This is the time period during which you have to pay taxes for the previous FY. The AY is also shown as “AY 2022-23”.

The deadline to file taxes by the taxpayers not subject to tax audits for the AY 2022-23 is July 31st, 2022. For other taxpayers to whom audit is applicable, the return filing due date is October 31st, 2022.

Where to report cryptocurrency gains income Tax Return (ITR) forms?

AY 2022-23 (Covers cryptocurrency activity from April 1st, 2021 to March 31, 2022).

The 2022 Finance act explicitly requires cryptocurrency profits to be subject to a 30% flat tax rate effective April 1, 2022. It is important to note that this time period is outside of the current AY 2022-23 which covers the period, April 1, 2021, to March 31, 2022.

That said, the conservative approach is to follow the new rules (even prior to the effective date) and subject your cryptocurrency activity to the 30% tax rate in the AY 2022-23.

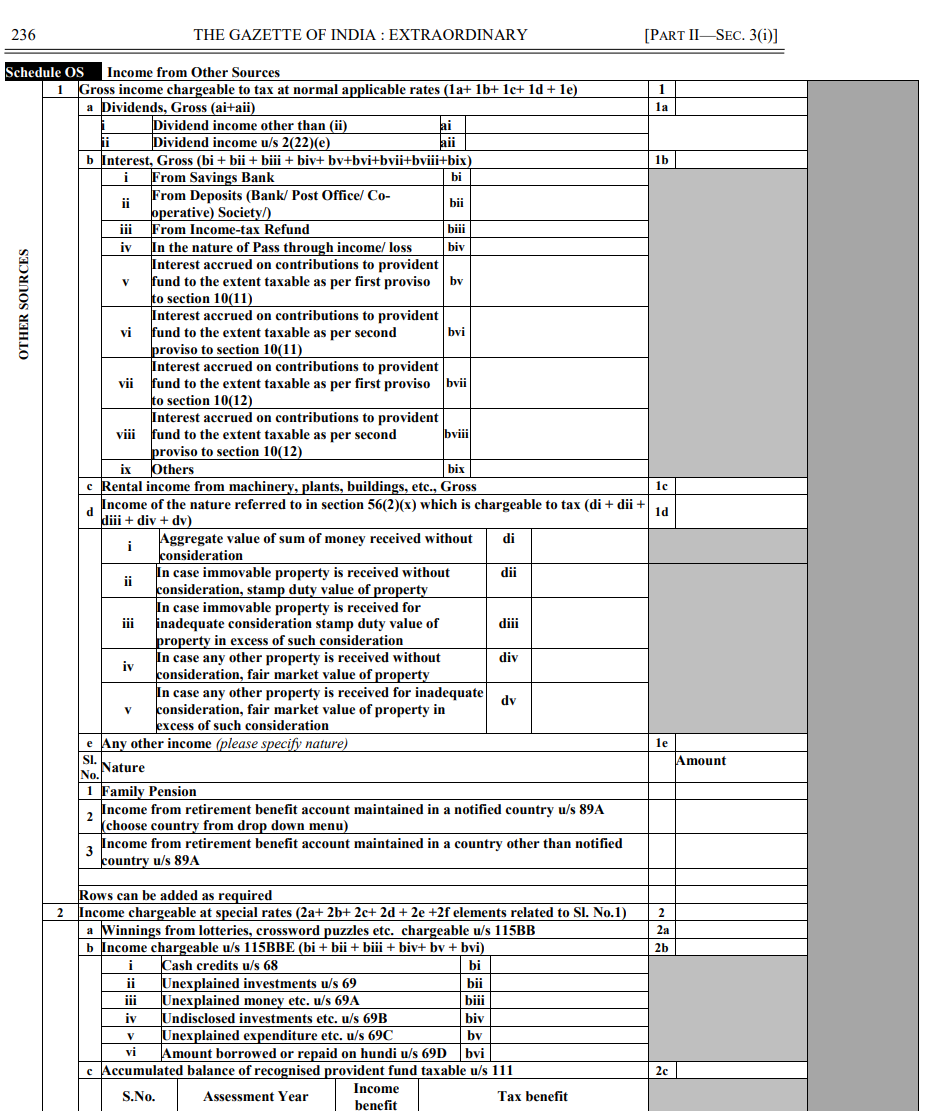

The AY 2022-23 ITR forms don’t have any dedicated schedules or lines to report your cryptocurrency activity. However, you could use, 2022-23 AY, ITR-2, Schedule OS, line 2s to report cryptocurrency gains. This will subject the profits to the 30% tax rate proactively.

We highly recommend consulting with your tax adviser to evaluate how you should treat cryptocurrency and where to report the activity for the AY 2022-23.

AY 2023-24 (April 1st, 2022 to March 31, 2023 cryptocurrency activity)

Cryptocurrency profits from Apr 1, 2022 to March 31, 2023, will definitely be subject to the 30% tax rate mandated by the Finance act. Most likely, the Income Tax Department (ITD) will update the AY 2023-24 ITR forms to report your cryptocurrency income separately in the future.

How to use CoinTracker as an accountant

What CoinTracker does

CoinTracker is a data aggregation tool that connects with your client’s cryptocurrency exchanges, wallets, blockchain, etc., and produces a gain/loss report for tax purposes. Without a tool like CoinTracker, it is virtually impossible to reconcile all the cryptocurrency transactions and produce gain and loss reports.

Workflow

Using CoinTracker with your client is an easy process:

- Direct your client to signup for an account at CoinTracker.

- Have your client connect read-only access to their crypto exchanges, wallets, and blockchains. If your client has any issues or needs help with this process, our customer service team is available to help.

- Have your client invite you to view their account so you can see the annual cryptocurrency gains and losses.

If you have any questions or comments about crypto taxes let us know on Twitter @CoinTracker.

CoinTracker integrates with 400+ cryptocurrency exchanges, and 8,000+ blockchains, and makes crypto tax calculations and portfolio tracking simple.

Disclaimer: This post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.