Are you confident in accurately reporting cryptocurrency earnings on your tax returns?

How to Optimize Your Cryptocurrency Taxes with Capital Gains & Losses

With 15 minutes of effort, you can save thousands if not more on your cryptocurrency taxes depending on your personal situation.

October 4, 2019 · 3 min read

Cryptocurrency taxes can be easy to gloss over, especially when your portfolio is down. This, however, is the optimal time to understand the basics of how cryptocurrency taxation works so that you can ensure that you are being smart about tax planning. With 15 minutes of effort, you can save thousands if not more depending on your personal tax situation.

Tax Overview

Per IRS notice 2014-21, virtual currencies are taxed as “property.” Therefore, general tax rules applicable to property should also be applied to cryptocurrency transactions. If you are a cryptocurrency investor, gains and losses are generally taxed as capital gains and losses (as opposed to ordinary gains and losses). In any given tax year, you pay capital gains taxes on your net capital gains. On the other hand, a smart investor can deduct net capital losses from their income. Let’s looks at how this works.

How Net Capital Gains and Losses are Calculated

The IRS uses a unique procedure to calculate your net capital gain/loss in any given year. It boils down to three steps:

- Short-term capital gains (STCG) are netted with Short-term capital losses (STCL)

- Long-term capital gains (LTCG) are netted with Long-term capital losses (LTCL)

- The results of steps 1 and 2 are netted against each other to arrive at short-term or long-term net capital gain or loss

Let's look at an example:

In 2019, Aurora sold 1 bitcoin for $10,000. She purchased it on October 2, 2017 for $4,000. In the same tax year, she also sold 30 ether for $8,000 which she purchased on October 5, 2019, for $20,000. In addition to crypto, she also has $1,000 of long-term capital gains coming from selling Google stocks. Applying the IRS’ methodology:

- LTCG on bitcoin = $10,000 – $4,000 = $6,000

- LTCG on Google stock = $1,000

- Total LTCG = $6,000 + $1,000 = $7,000

- STCL on ether = $8,000 – $20,000 = - $12,000

- Net STCL = $7,000 – $12,000 = - $5,000

Aurora ends the year with a $5,000 net short-term capital loss.

But wait, it gets even better. Of this $5,000 net short-term capital loss, Aurora can deduct $3,000 worth of losses in 2019 tax year and better yet, she can also carry forward the remaining $2,000 loss to future tax years.

In essence, Aurora completely sheltered her bitcoin and Google stock capital gains from taxation, reduced her taxable income by $3,000, and carried forward losses to continue using in future tax years by spending 15 minutes on CoinTracker.

What's Good & Bad about Capital Gains?

Here is the good news: capital gains are subject to preferential tax rates under the IRS tax code. For example, in 2020, Aurora could have a net capital gain of $1,000 or $1M, or even $10M, but she will only have to pay a maximum of 20% regular income tax on that gain (compare this to the maximum tax rate of ordinary gains at 37%!).

The bad news: according to IRS rules, you can only claim a maximum net capital loss up to $3,000 in any given tax year. Going with the example shown above, Aurora only gets to claim a $3,000 capital loss against income in 2019 despite having a $54,000 actual net short-term capital loss. She will have to wait until the next tax year to claim the remaining $21,000 short-term capital loss.

Note: you can generate an unlimited amount of capital loss in a given tax year and you can use those capital losses to offset an unlimited amount of capital gains. However, in any given tax year, the maximum amount of net capital loss (after going through netting procedures described above) you can deduct on your tax return is $3,000. Your net capital loss above the $3,000 threshold is carried forward to future years.

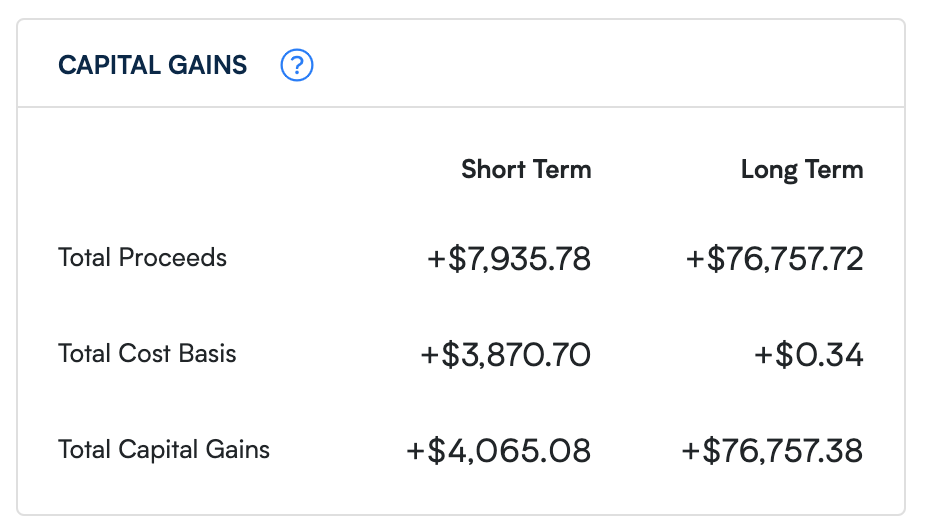

Annual net capital gain/loss calculations can get especially complicated with cryptocurrency. Luckily, crypto capital gain calculations can be automated with tax software like CoinTracker.

The CoinTracker dashboard shows your short-term and long-term capital gains; you can also download your IRS forms like (Form 8949 and Schedule D).

CoinTracker helps you calculate your crypto taxes by seamlessly connecting to your exchanges and wallets. Questions or comments? Reach out to us @CoinTracker.

Disclaimer: this post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.