How the IRS is Approaching Cryptocurrency Compliance: Updates from the IRS Chief Counsel

Oct 24, 2019・4 min read

On October 17, 2019, Michael J. Desmond (Chief Counsel, Internal Revenue Service) spoke at The Urban Institute on Cryptocurrency and Tax Administration (full video).

Here is a breakdown of the speech highlights and updates on the cryptocurrency tax space.

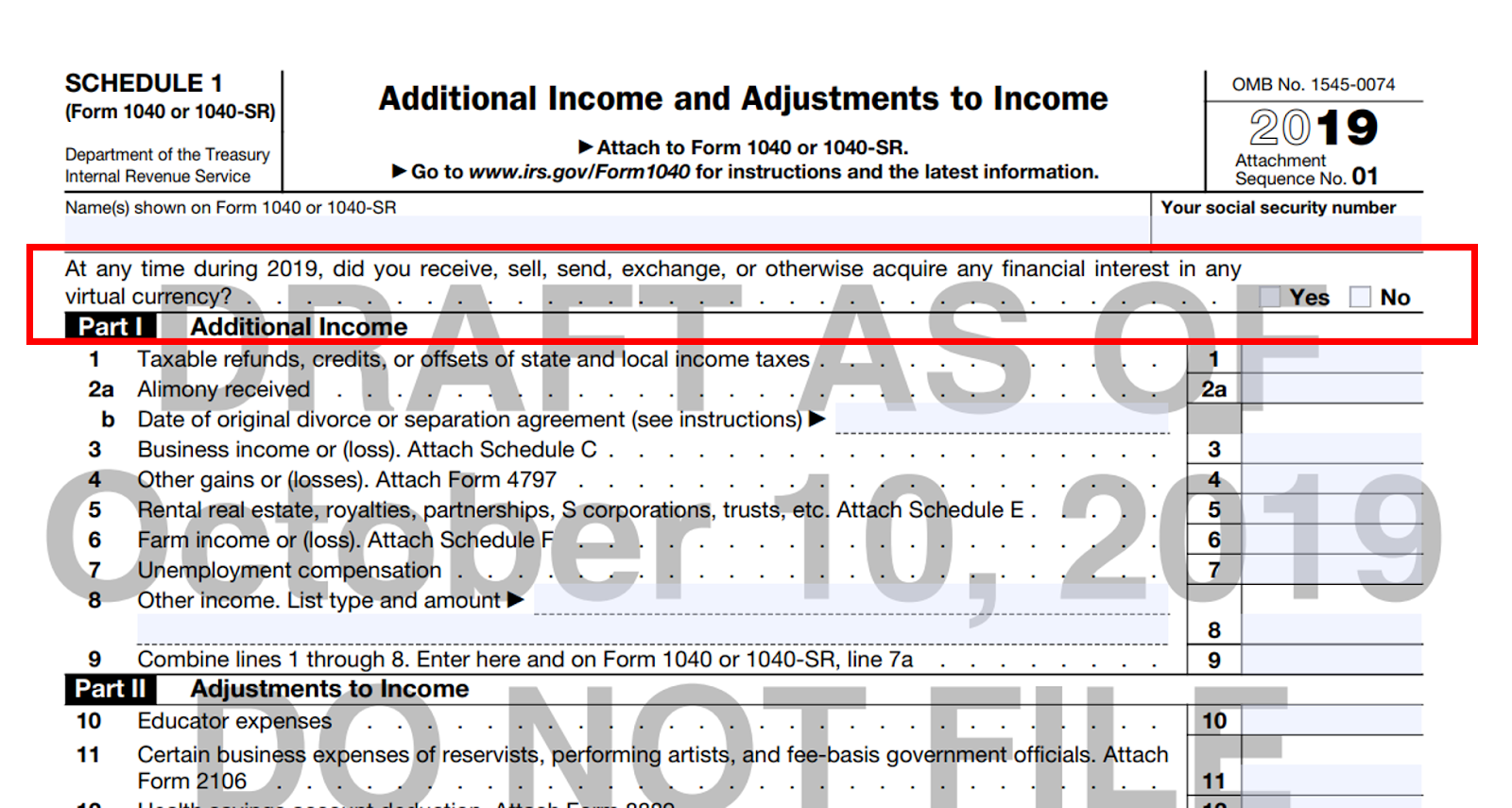

Cryptocurrency Question on 2019 Schedule 1

According to Desmond, the IRS receives approximately 150 million tax returns annually. Various sources report that there are about 7-11% of adults in the US with some sort of economic affiliation with virtual currencies, indicating that the IRS should receive roughly 12 million tax returns with some sort of cryptocurrency transactions. However, the amount of returns received with such transactions is far fewer than that.

To combat cryptocurrency under-reporting, the IRS has introduced a new draft of the 2019 IRS Form 1040, Schedule 1 which includes a question about cryptocurrency to all US taxpayers. The inclusion of the above question will enable the IRS to find out how prevalent crypto taxpayers are in the economy.

The IRS took a similar approach with the yes/no question on Part III of Schedule B which asks taxpayers whether they have any financial interest in any offshore accounts. The foreign financial accounts program has been very successful in gathering a lot of useful data, and according to the chief counsel, the service is attempting to replicate the same data gathering mechanism in the crypto space.

Cryptocurrency is a high priority for the IRS because there is a high degree of non-compliance as shown in the data above. The IRS is not dead set on perfect compliance — it’s main focus is to move taxpayers from reporting nothing, to report something on tax returns.

2025

Crypto Tax

Guide is here

CoinTracker's definitive guide to Bitcoin & crypto taxes provides everything you need to know to file your 2024 crypto taxes accurately.

“Cubby-hole” Approach

In the coming months, per Desmond, the IRS will tackle the cryptocurrency compliance space in two ways: guidance and enforcement. According to his comments, the IRS past and upcoming crypto guidance will take a “cubby-hole” approach.

What does this mean? Currently, the IRS is not planning on coming up with new set of laws applicable specifically to cryptocurrency transactions. Instead, it continues to believe that cryptocurrencies are closely aligned with “property” under the tax code and rules applicable to property will continue to apply to cryptocurrency transactions (more on how cryptocurrency taxes work). Although property treatment causes friction for cryptocurrency as a medium-of-exchange, it offers more clarity and comfort to lawmakers and enforcement agencies like the IRS. This is because the tax rules applicable to property are well defined in the tax code, so taxpayers and practitioners can rely on an extensive history of case law to make good faith assumptions on how to deal with cryptocurrency transactions.

The IRS also understands that emerging technologies evolve faster than the guidance they provide. Old laws, regulations and case laws related to property transactions may not be a perfect fit for new situations arising in the cryptocurrency world. These sometimes pose challenges in terms of issuing, updating & enforcing rules, and the IRS is aware of that.

When is the Guidance Effective?

Both taxpayers and practitioners have asked whether the new IRS guidance issued on October 9, 2019 is applicable retroactively or only going forward. According to the comments made by the chief counsel, the new guidance merely elaborated on the original Notice 2014-21. Therefore, in the eyes of the IRS, these new rules have already been active since 2014.

This presents some challenges to taxpayers who decided not to recognize any income for forks based on “lack of guidance” premise in the past years. Ideally, they would have to go back and amend the returns to reflect the new guidance.

Other Miscellaneous Items

Airdrops and Hard Forks

Recently issued FAQs imply that airdrops are generally followed by hard forks. This is not the industry norm. In fact, in many cases, airdrops and forks are two unrelated events. The IRS acknowledges that there is a mismatch between the IRS interpretation of these concepts and the actual industry practices. The service is open to hear more feedback and comment on this issue.

Under-reporting

The IRS is trying to make 1099-K reporting more stringent for US based crypto exchanges. In their view, although 1099-Ks do not report anything truly meaningful for taxpayers who want to calculate capital gains/losses, they significantly increase the compliance rate.

The biggest problem the IRS is facing with regard to cryptocurrency is that taxpayers are not reporting anything at all. IRS education letters and the new cryptocurrency question on Schedule 1 are mainly to move taxpayers from reporting nothing to reporting something. The service also understands that there are complex situations that the existing laws do not provide enough guidance for. In these cases, the IRS is willing to work with taxpayers who report something and figure out the proper tax treatment on a case-by-case basis.

Property

The IRS wants to stick with the property treatment for cryptocurrencies. If the congress wants to change that treatment, the IRS is ready to react.

Foreign Reporting

More guidance on FBAR (FinCEN 114) and FATCA (IRS Form 8938) will arrive in the coming months. Currently, there is no legal requirement to report overseas virtual currency transactions on FBAR (FinCEN 114 Form).

CoinTracker helps you calculate your crypto taxes by seamlessly connecting to your exchanges and wallets. Questions or comments? Reach out to us @CoinTracker

Disclaimer: this post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.