Are you confident in accurately reporting cryptocurrency earnings on your tax returns?

Cryptocurrency Taxes in Canada

CoinTracker can help you track your cryptocurrency, maintaining proper transaction records, and minimize your tax burden along the way.

April 23, 2019 · 3 min read

By CoinTracker and Eric Cohen (FL Fuller Landau)

On December 9, 2018, Gerald Cotten, founder and CEO of Canadian cryptocurrency exchange QuadrigaCX, reportedly died while traveling in India at the age of 30. Cotten reportedly maintained sole possession of the exchange’s wallets and as a result, with his death over 115,000 users lost access to an estimated $145 million (C$190 million) in cryptocurrency.

Unfortunately, stories of lost and stolen exchange funds are far too common. In the past 18 months alone there have been at least five major attacks on cryptocurrency exchanges resulting in over $500 million (C$650 million) in losses. The good news is you can use tools like CoinTracker to help you manage these situations by keeping tabs on your coins, maintaining proper transaction records, and minimizing your tax burden along the way. Here are three tips for protecting yourself and your funds:

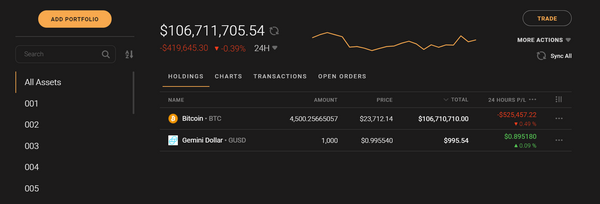

1. Maintain independent records: keep track of your transaction history as you go. If an exchange shuts down, you may be left unable to recreate your transaction history. Use a non-custodial portfolio tracker like CoinTracker to ensure you always have backup records of your transactions. CoinTracker can automatically sync your data via API from exchanges such as Coinsquare, Shakepay, Coinbase, and others

2. Self-custody: minimize funds kept on centralized exchanges. If you do not control your private keys, do not assume your funds are safe — they are only as secure as the company holding onto them. Keep any funds you don’t need immediately off-exchange on a hardware or local wallet and track them securely. CoinTracker shows you the percentage of your funds held on exchanges vs. off-exchange

3. Claim losses: if you have losses from stolen or lost funds, claim them! You can minimize your tax burden by claiming any stolen funds. If you are a QuadrigaCX user and haven’t claimed your losses yet, make sure to file by the April 30, 2019 Canadian tax deadline (or go back and amend if you have already filed)

Confused about Canadian cryptocurrency tax rules? Here’s how it works:

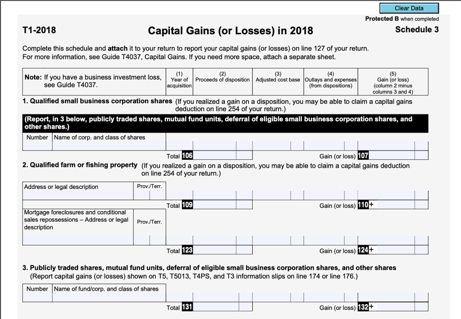

- The Canadian Revenue Agency (CRA) considers virtual currency transactions taxable, which means you will need to complete a CRA Schedule 3 Capital Gains report using the Adjusted Cost Base (ACB) method (CoinTracker does this for you automatically). Also, be aware that these transactions may be viewed as income and not capital. Consult your tax advisor to be sure

- If you held foreign property (including cryptocurrency) greater than CAD 100,000 in value during any time during the year, you may also be required to fill out a T1135 — Foreign Income Verification Statement (CoinTracker also calculates the numbers you need to complete this form)

- If you have cryptocurrency losses, they can offset other capital gains or are eligible to be carried forward and applied against future capital gains. A knowledgeable accountant from a firm like FL Fuller Landau can also help with tax advice or tricky accounting questions around cryptocurrency

For more information see how cryptocurrency taxes work in Canada. Then head over to CoinTracker or speak to your FL tax advisor to get your crypto taxes filed today!

CoinTracker helps you calculate your crypto taxes by seamlessly connecting to your exchanges and wallets. Questions or comments? Reach out to us @CoinTracker.

Disclaimer: this post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.