Ways to Lower Your Crypto Tax Bill: Which Cost Basis Method is Best?

Sep 6, 2022・4 min read

In 2014, the IRS released guidance that cryptocurrencies are taxed as property. Five years later, in 2019, they updated the guidance to specify which types of accounting methods are allowed for calculating your cryptocurrency capital gains and losses. Understanding these rules and how you can take advantage of them can result in enormous tax savings.

Accounting 101

Before diving into the tax savings, it’s important to understand some accounting basics. Cost basis is the total fair market value of your currently held (crypto) assets at the time you acquired them. Basis, along with proceeds (the fair market value of your assets at the time they are sold), are used to calculate your capital gain or loss.

Capital Gain/Loss = Total Proceeds – Cost Basis

In the US, since cryptocurrency is taxed as property, you will be taxed on your net capital gain or loss.

2025

Crypto Tax

Guide is here

CoinTracker's definitive guide to Bitcoin & crypto taxes provides everything you need to know to file your 2024 crypto taxes accurately.

Cost Basis Methods

There are various ways to calculate your capital gains based on the cost basis method you choose. Critically, cost basis affect how your capital gains are calculated. As crypto assets purchased at different times can have different cost basis, your capital gain will change depending on which unit of your asset you decide to sell (from an accounting perspective). This is determined by your cost basis method and is why choosing the right cost basis method can either save you or cost you thousands on your tax return.

Specifically, the IRS outlines that there are two acceptable cost basis methods: First In, First Out and Specific Identification.

First In, First Out (FIFO)

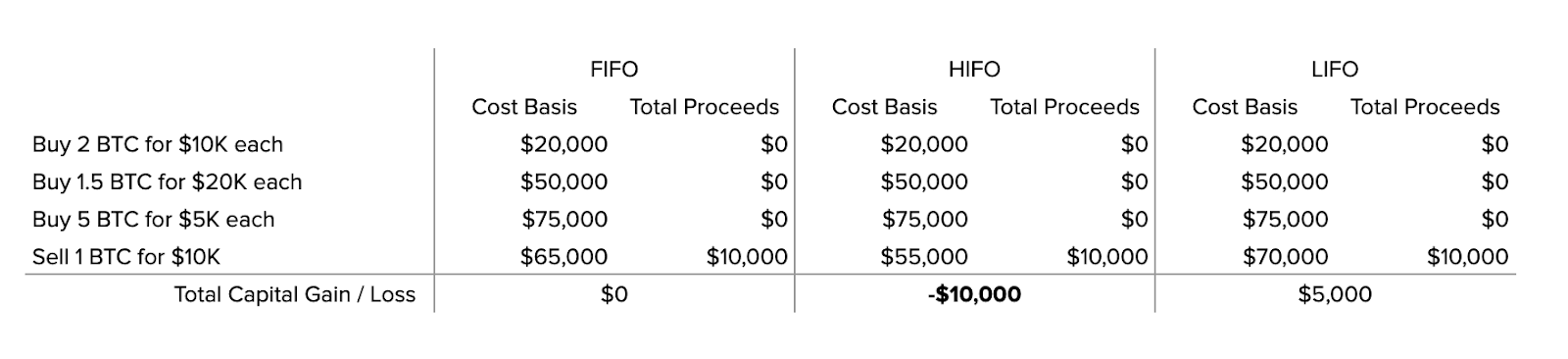

The simplest cost basis method is First In, First Out (FIFO). FIFO means that the first unit you purchase is the first unit that is sold from a tax perspective. FIFO is great from a simplicity perspective because it is the most straightforward accounting method. Additionally FIFO will always spend your longest held assets first which can be beneficial in taking advantage of long term capital gains rates (which are lower than short term capital gains rates).

Specific Identification

Specific Identification allows the taxpayer to choose which specific asset unit is being disposed with each transaction. These can be arbitrarily selected by the taxpayer, or follow a pattern like Last In, First Out, or Highest In, First Out. According to the IRS virtual currency FAQs (October 9, 2019):

"You may identify a specific unit of virtual currency either by documenting the specific unit’s unique digital identifier such as a private key, public key, and address, or by records showing the transaction information for all units of a specific virtual currency, such as Bitcoin, held in a single account, wallet, or address. This information must show (1) the date and time each unit was acquired, (2) your basis and the fair market value of each unit at the time it was acquired, (3) the date and time each unit was sold, exchanged, or otherwise disposed of, and (4) the fair market value of each unit when sold, exchanged, or disposed of, and the amount of money or the value of property received for each unit."

This can be tricky to calculate manually, however tax software like CoinTracker produces the detailed records you need to meet the specific identification requirements by the IRS.

Last In, First Out (LIFO)

Last In, First Out (LIFO) is another cost basis method that does the opposite of FIFO. Instead of selling the units that you have held the longest, LIFO prioritizes the sale of units purchased most recently. LIFO can create greater short-term capital gains than FIFO, however may be beneficial in cases where you are doing high frequency trading or when the underlying assets have been increasing in value over a long period of time.

Highest In, First Out (HIFO)

Highest In, First Out (HIFO), is the cost basis method that typically results in the lowest tax bill and is the default cost basis method in CoinTracker. HIFO does not prioritize units based on when they were purchased, but instead prioritizes units on how much it cost to acquire them. This means that your assets that have the highest cost basis are the ones that are first sold. Given that your capital gains are equal to your total proceeds (how much you made from a sale) minus your cost basis, a larger cost basis means your capital gains are minimized.

Example

Adjusted Cost Base (ACB) 🇨🇦

Adjusted Cost Base, or ACB, is a cost basis method required by the Canadian Revenue Agency. While the calculations are a bit more complex than FIFO, HIFO, and LIFO, the general idea is that you average the basis of each asset across all units. CoinTracker can perform all of these calculations for you. Learn more about Canadian cryptocurrency taxes.

Share Pool 🇬🇧

Share Pooling, also known as share-matching, is a UK specific cost basis method that is required by HMRC. When you spend, sell, or trade cryptocurrency, you will be treated as disposing them in the following order:

- Same Day Rule: coins acquired on the same day as the disposal are consumed first in an average pool

- Bed and Breakfasting Rule: coins acquired in the 30 days following the day of disposal

- Pool rule: all other coins purchased, price averaged

CoinTracker has you covered when it comes to Share Pool and you can read more about how crypto tax works in the United Kingdom.

CoinTracker: Crypto Taxes Made Simple

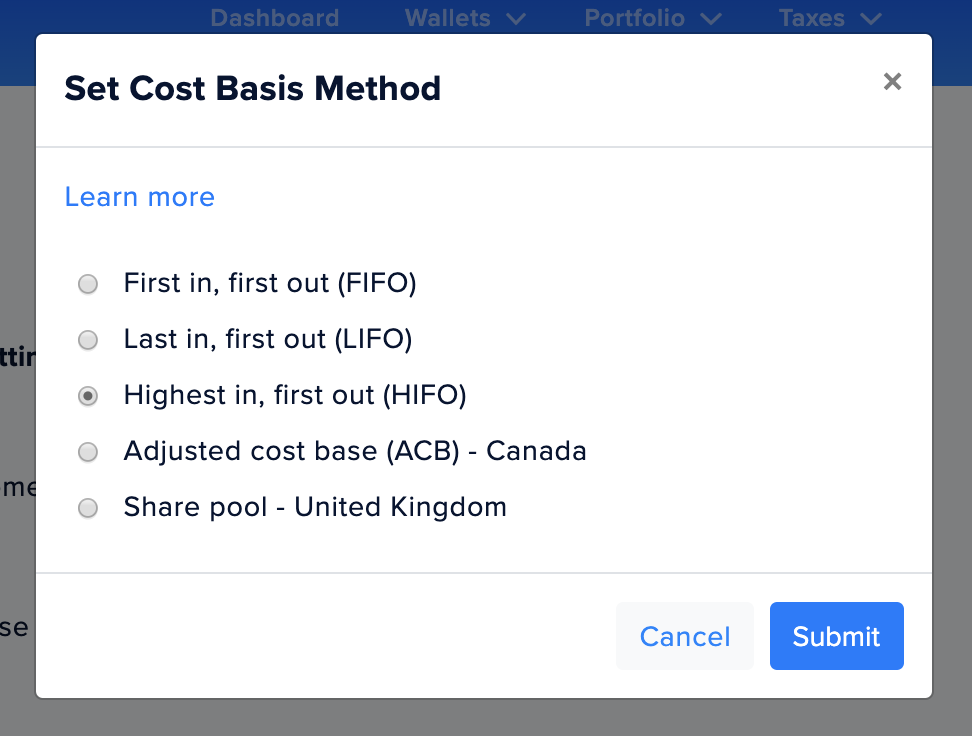

When it comes to cost basis, there’s no one-size-fits-all solution, but any good tax software should be able to help you make the right choice. CoinTracker supports FIFO, LIFO, HIFO, ACB, and Share Pool when it comes to your cost basis. CoinTracker’s Tax Loss Harvesting Dashboard will also highlight any opportunities you have to save on your crypto taxes.

Once you’ve connected all your accounts to CoinTracker, you can generate your tax reports in minutes. Over 100,000 users have used CoinTracker to optimize their taxes and claim over $600M in capital losses. Get started today at www.cointracker.io.

Let us know your questions and feedback on Twitter @CoinTracker

Disclaimer: this post is informational only and not intended as tax advice. For tax advice, please speak with a tax professional.